Colophon

The Freeze is a monitoring-station readout, not a verdict. It plots published numbers and sourced figures and refuses the leap to intent. If a claim here is not a plotted series or a cited release, it should not be here.

SOURCES

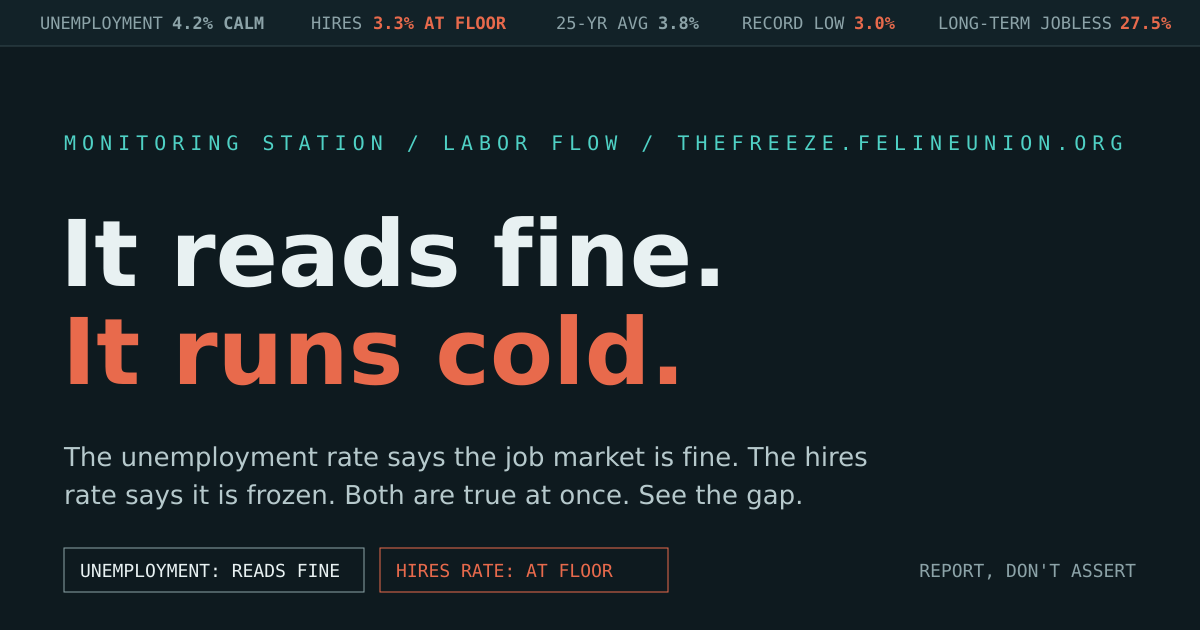

· BLS JOLTS — hires rate, quits rate, job openings rate (series since 2001)

· BLS CES — nonfarm payroll change

· BLS CPS — unemployment rate, labor-force participation, long-term-unemployed share

· BLS LNS — prime-age (25–54) employment-to-population ratio

· StatCan LFS — Canadian employment rate

· OECD — cross-country comparison context

Honesty line: readings are annual averages, shapes are exact, decimals are approximate. The hires-rate series begins in 2001 because JOLTS begins in 2001; no earlier hires line exists and none is drawn.

Report, don't assert. · A Feline Union property.